Hedging with EVAA (Lending)

TONCO x EVAA hedging strategy

Entering unprotected LP positions, especially within a narrow range, can be high-risk. While APR on TONCO can be as high as 3-digits on GRAM/USDT pair, the impermanent loss can eat into your profits.

It may be a good idea to hedge the position in order to protect your investment.

A hedged LP position involves using additional funds as collateral to borrow the volatile asset like GRAM, using the EVAA Finance protocol (hedging the downside risk on price decrease).

Example

You have $15,000 and want to open a position in the GRAM/USDT pair on TONCO DEX. Assuming the APR for a GRAM/USDT pair is 100% and Gram (prev. Toncoin) is traded at 5 USDT.

You put 1500 GRAM and 7,500 USDC into a liquidity pool on TONCO DEX. Let's say you put range between 4.5 and 5.5. As long as the GRAM price stays within your designated range, you’ll earn trading fees.

One day, the price of GRAM drops beyond your range to 4 USDT. You end up with a position consisting of ≈ 3,060 GRAM (as the ratio changes along the way, you end up with slightly more than 2x GRAM) and 0 USDT. You are now fully exposed to the GRAM price and experience permanent loss.

After selling the tokens received for providing liquidity for 30 days while being in-range, the cumulative yield stands at 1,232 USDT (calculated as 7,500 * 2 * 100% / 365 * 30). You decide to stop providing liquidity.

If you sell the 3,060 GRAM at 4 USDT each and combine the proceeds with the 1,232 USDT, you’ll see a total loss of 1,528 USDT ((3,060 * 4 + 1,232) - 7,500 * 2) due to impermanent loss.

Hedging vs. No Hedging

• Without Hedging

If you had opened the original position without any hedging ($15,000: 7,500 USDT + 1,500 GRAM), you would have ≈3,060 GRAM and 0 USDT. If you decide to lock in your loss and withdraw 3,060 GRAM, you would receive:

— 3,060 * 4 = $12,240 (if the price of GRAM dropped to $4)

— Trading fees ($1,232 from the example above)

The total would be:

$12,240 + $1,232 = $13,530, a -10.18% loss

• With Hedging on EVAA (the downside risk on price decrease)

In the hedged scenario, you supply 10,000 USDT to borrow the volatile asset (1,500 GRAM) from EVAA. After the GRAM price drops, you withdraw ≈ 2,040 GRAM. You sell 540 GRAM for $2,160 and repay the 1,500 GRAM borrowed from EVAA. You also retrieve your $10,000 collateral from EVAA and have an additional $2,500 from the initial GRAM-USDT trade at $5.

The total would be:

— $2,160 (from the sale of 540 GRAM at $4)

— $2,500 (from the remaining GRAM traded at $5)

— $10,000 (collateral returned)

This gives you:

$2,160 + $2,500 + $10,000 = $14,660, plus:

— Trading fees ($1,232 from the example above)

— EVAA net APR (+6.92%, which equals $58)

The total would be:

$14,660 + $1,232 + $58 = $15,950, a +6.4% profit

This means that by hedging, you have completely mitigated the loss from the drop in the GRAM price and made a profit from the position.

Step-by-step strategy for hedging

Here’s a step-by-step strategy for hedging the downside risk of a GRAM price decrease.

There is a symmetrical strategy that aims to protect the gains in case the asset price goes up. Instead of borrowing GRAM, you’d either buy it and borrow USDT against it.

1. Supply USDT to EVAA

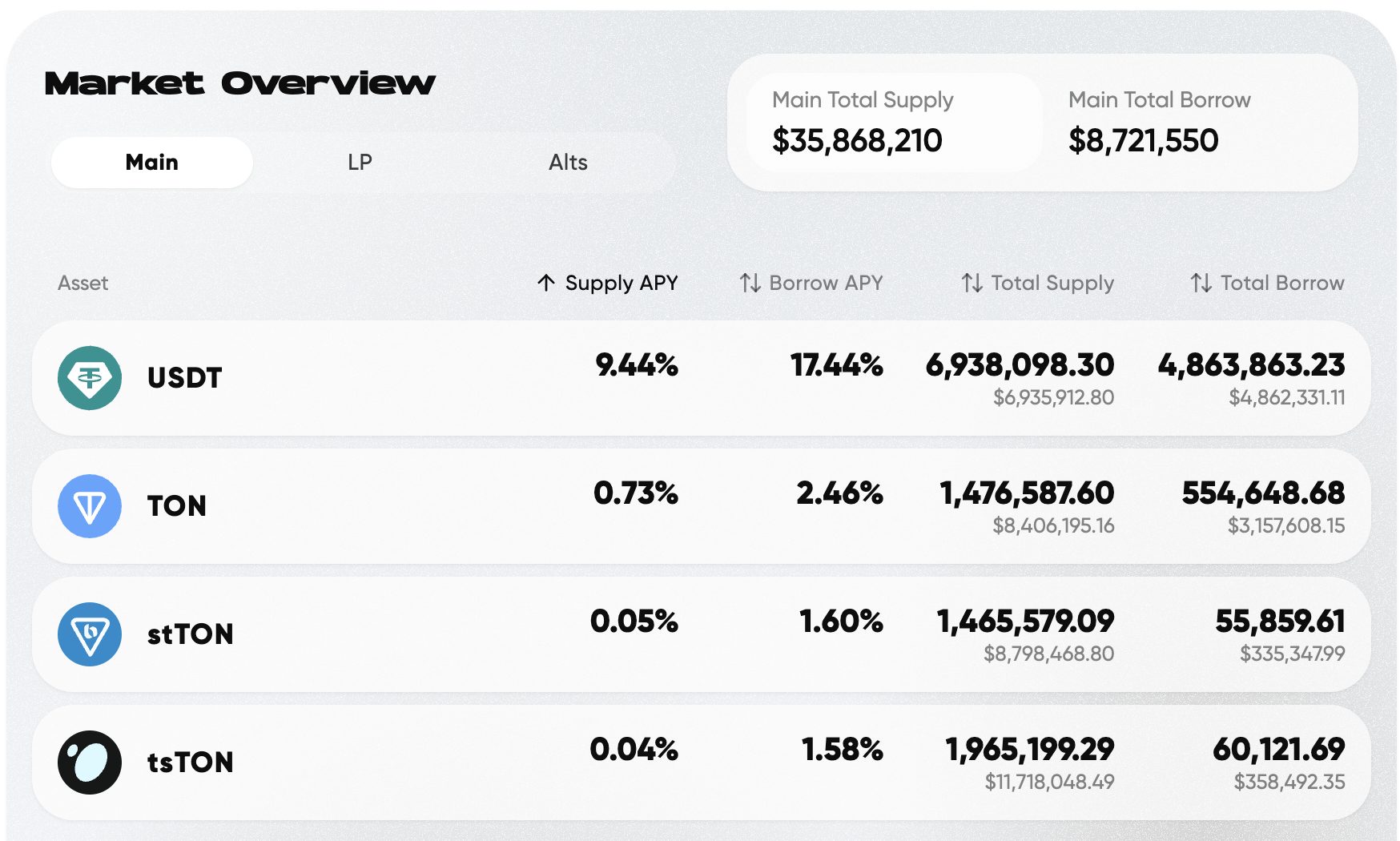

Start by supplying $10,000 worth of USDT to EVAA. As of December 18th, you’ll earn an APR of over 9.4% on USDT.

EVAA markets as of Dec 18th, 2024

2. Borrow GRAM

Pledge your $10,000 USDT as collateral to borrow 1,500 GRAM (assuming the price of 1 GRAM = 5 USDT). You will pay a borrowing APR of around 2.4% on GRAM. Your net APR on EVAA will be ≈ +6.9% (as of December 18th).

3. Open LP position

You now have your initial $5,000 in USDT plus the 1,500 GRAM borrowed from EVAA.

Open an LP position with 5,000 USDT and 1,000 GRAM (worth $5,000). This brings your total position value to $10,000. After opening the position, you can sell the remaining 500 GRAM you borrowed, converting it into 2,500 USDT.